Total Produce

TIP

Re: Total Produce

Ze leveren uiteraard ook aan Whole Foods & die zijn blijkbaar heel tevreden...

15% vd omzet komt uit International (USA & India), zo'n 12% EBITA. De M&A groei komt wel vnl. uit America.

Ik zie niet echt een probleem...

http://www.theshelbyreport.com/2017/04/ ... d-winners/

Distinguished Service

The Oppenheimer Group (Oppy), for its partnership in developing key programs with Whole Foods Market and for its commitment to customer service, transparency and business planning that supports Whole Foods Market store produce companywide.

15% vd omzet komt uit International (USA & India), zo'n 12% EBITA. De M&A groei komt wel vnl. uit America.

Ik zie niet echt een probleem...

Re: Total Produce

Eén order van 73.858 stuks @ 2€ om 17:32. Toen nieuws van Amazon bekend werd was er geen reactie in de koers.

Ter vergelijking Ahold dook al om laag na 15:00.

Ter vergelijking Ahold dook al om laag na 15:00.

Re: Total Produce

TOT levert net aan supermarkten hè. Denk niet dat Amazon zelf appels gaat telen.

Re: Total Produce

Blijkbaar vandaag resultaten geweest :O

mail niet bekeken & agenda fout ingevuld

mail niet bekeken & agenda fout ingevuld

soit, ziet er zeker niet slecht uit opt eerste zicht. Tis al laat dus zal voor int weekend zijnTOTAL PRODUCE CONTINUES STRONG GROWTH

Revenue up 12.2% to €2.15 billion

Adjusted fully diluted EPS up 10.1% to 6.78 cent

Adjusted EBITDA up 9.5% to €52.8m

Adjusted EBITA up 12.0% to €42.5m

Adjusted profit before tax up 11.8% to €39.0m

Interim dividend up 10.0% to 0.8906 cent per share

Continues to target increased full year adjusted earnings per share in the upper half of the previously announced range of 12.0 to 13.0 cent per share

...

Group continues to be cash generative with operating cashflows of €33.3m (2016: €32.5m) before normal seasonal working capital outflows.

Re: Total Produce

Deze klimt langzaamaan ook richting fair value.

Vandaag de +100% bereikt in mn port & als ik puur kijk naar de fair value zou ik kunnen verkopen. Maar langs de andere kant is de groei spectaculair & is de trend naar gezond eten nog lang niet gedaan, daarnaast is het een versnipperde sector waar ze 1 van de marktleiders zijn & dus in principe moeten kunnen profiteren van consolidatie in de sector.

Vandaag de +100% bereikt in mn port & als ik puur kijk naar de fair value zou ik kunnen verkopen. Maar langs de andere kant is de groei spectaculair & is de trend naar gezond eten nog lang niet gedaan, daarnaast is het een versnipperde sector waar ze 1 van de marktleiders zijn & dus in principe moeten kunnen profiteren van consolidatie in de sector.

Re: Total Produce

Die van mij zijn al buiten. Waardering is fair en had elders cash nodig. Als je in dezelfde sector wil blijven, kan je ook eens naar het (veel kleinere) Produce Investments kijken.

Re: Total Produce

Ziet er interessant uit qua cijfers, ga het nader bekijken.

wel enkele minpunten;

- microcap

- 97% sales in de UK

- bijna volledige omzet uit mindere exoten; aardappelen & 'narcissen' (zolang het maar geen tulpenbollen zijn

-

anonymous9

Re: Total Produce

¿Qué pasó?

Re: Total Produce

toch nog ff tijd gevonden...

Ze hebben daar toch een probleem met hun werkkapitaal, stijgt al 5 jaar op rij. laatste jaar zelfs met meer dan £ 8M.

Ondanks zware investeringen (aankoop packing facility van 6,1M)toch een FCF van meer dan £ 8M (incl. WC).

marktcap= £50M

netdebt = £ 28M (zou moeten zakken als werkkapitaal terug stabiliseert?!)

fair value = +- £ 85M (15x FCF van 7M, min 20M aan schulden)

Ze hebben daar toch een probleem met hun werkkapitaal, stijgt al 5 jaar op rij. laatste jaar zelfs met meer dan £ 8M.

Ondanks zware investeringen (aankoop packing facility van 6,1M)toch een FCF van meer dan £ 8M (incl. WC).

marktcap= £50M

netdebt = £ 28M (zou moeten zakken als werkkapitaal terug stabiliseert?!)

fair value = +- £ 85M (15x FCF van 7M, min 20M aan schulden)

Re: Total Produce

Ha. Ik maakte net dezelfde opmerking bij Poldermol.

Ligt vooral aan de evolutie van de receivables, maar die lagen in 2008 (zo ver ben ik gaan terugkijken) zeer laag in verhouding tot de payables (£16,8m aan receivables tegenover £25,9m aan payables), terwijl ze nu meer in lijn liggen. In die zin is het hogere werkkapitaal misschien eerder een normalisatie dan een onrustwekkende stijging.

Ligt vooral aan de evolutie van de receivables, maar die lagen in 2008 (zo ver ben ik gaan terugkijken) zeer laag in verhouding tot de payables (£16,8m aan receivables tegenover £25,9m aan payables), terwijl ze nu meer in lijn liggen. In die zin is het hogere werkkapitaal misschien eerder een normalisatie dan een onrustwekkende stijging.

-

anonymous9

Re: Total Produce

Ik legde het zo uit aan mijn lezertjens:

Should you be worried about the continuous need for working capital investments?

A large part of the operating cash flow was invested in the working capital position. Whilst 1.5M GBP was explained by Produce Investments paying some of the outstanding invoices, the total amount of receivables and inventory levels increased as well.

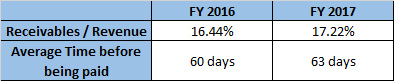

This isn't necessarily bad. As you might remember, PIL delivers their products to retail chains and those don’t really pay ‘on the spot’. So as the revenue increases, the total amount of outstanding invoices will increase as well. In fact, the increase of the receivables wasn’t exorbitantly high, as you can see in the next image.

So, yes, PIL has to wait a little bit longer to see their invoices being paid, but the difference isn’t very alarming at all. On top of that, it’s able to benefit from an ‘invoice finance’ facility (which probably is a straightforward ‘factoring’ agreement.

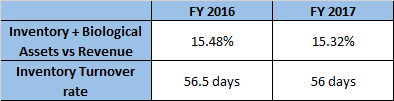

The higher investment in the inventory and biological assets level is actually justified (and very reasonable as well). Let’s compare the 2017 results with 2016.

So, the inventory turnover rate has actually decreased, although you have to take a certain seasonality effect into consideration as well. Produce Investments usually ends the year with relatively low inventory levels.

Should you be worried about the continuous need for working capital investments?

A large part of the operating cash flow was invested in the working capital position. Whilst 1.5M GBP was explained by Produce Investments paying some of the outstanding invoices, the total amount of receivables and inventory levels increased as well.

This isn't necessarily bad. As you might remember, PIL delivers their products to retail chains and those don’t really pay ‘on the spot’. So as the revenue increases, the total amount of outstanding invoices will increase as well. In fact, the increase of the receivables wasn’t exorbitantly high, as you can see in the next image.

So, yes, PIL has to wait a little bit longer to see their invoices being paid, but the difference isn’t very alarming at all. On top of that, it’s able to benefit from an ‘invoice finance’ facility (which probably is a straightforward ‘factoring’ agreement.

The higher investment in the inventory and biological assets level is actually justified (and very reasonable as well). Let’s compare the 2017 results with 2016.

So, the inventory turnover rate has actually decreased, although you have to take a certain seasonality effect into consideration as well. Produce Investments usually ends the year with relatively low inventory levels.

-

anonymous9

Re: Total Produce

En wat de schulden betreft, dit jaar gaan ze ook de site van een gesloten fabriek verkopen. Dus ik reken erop dat de YE net debt uitkomt op 21-22M GBP uitkomt, wat 1.5X EBITDA is.

Re: Total Produce

jup, had ik gelezen in het jaarraport. Enig idee wat die gaat opbrengen?

Ik had ruwweg geschat op een net debt van 20M.

enig idee waar ik het orderboek (in realtime) kan bekijken?