Roularta

TIP

Re: Roularta

Iemand enig idee of die https://storesquare.be een succes kan worden? Wordt flink wat geld tegenaan gegooid...

Re: Roularta

Aandeel heeft serieuze klappen gekregen de laatste tijd (na zwakke resultaten een tijd terug) maar gistere nog eens 6% er van af...

Wat ik me af vraag, hoe giet je die dividenduitkering van medialaan best in de GPV methode? Gewoon het dividend meerekenen dat betaald is (zoals in cashflowstatement)

Of deze eruit halen en waarderen volgens een SOTP?

"Aandeel in het resultaat van geassocieerde ondernemingen en joint ventures"

Dit gaat over verschillende minderheidsparticipaties, waarvan medialaan de grootste vormt. Hoe beoordeel je zoiets best vermits we geen FCF's kunnen berekenen op deze participaties?

http://www.roularta.be/sites/default/fi ... V16_NL.pdf

Wat ik me af vraag, hoe giet je die dividenduitkering van medialaan best in de GPV methode? Gewoon het dividend meerekenen dat betaald is (zoals in cashflowstatement)

Of deze eruit halen en waarderen volgens een SOTP?

"Aandeel in het resultaat van geassocieerde ondernemingen en joint ventures"

Dit gaat over verschillende minderheidsparticipaties, waarvan medialaan de grootste vormt. Hoe beoordeel je zoiets best vermits we geen FCF's kunnen berekenen op deze participaties?

http://www.roularta.be/sites/default/fi ... V16_NL.pdf

Re: Roularta

over de waardering van Medialaan. uit het rapport van Degroof een tijdje terug;

(gezien de mindere cijfers kan/zal die waardering nu lager liggen)

(gezien de mindere cijfers kan/zal die waardering nu lager liggen)

1) Buy the remaining 50% in Medialaan. This would enhance 2019e EPS by 24% on a normalized basis. It should also trigger a re-rating because of simplification, improved transparency, full ownership and control, and mass. This suggests a target price of at least EUR 46.

2) Sell the 50% stake in Medialaan. This would depress EPS by 67%, it would result in a target price of EUR 11.7 for Printed Media and net cash of EUR 32.0 p/s for an overall target price of EUR 44.

-

anonymous9

Re: Roularta

Ik neem het dividend mee in de berekeningen. Vorig jaar was het dividend lager, door de incorporatie van Mobile Vikings. Ik heb een paar weken terug er een artikeltje over geschreven. Het zit achter een paywall, maar hier een uittreksel:Umi schreef: ↑5 augustus 2017, 13:25 Aandeel heeft serieuze klappen gekregen de laatste tijd (na zwakke resultaten een tijd terug) maar gistere nog eens 6% er van af...

Wat ik me af vraag, hoe giet je die dividenduitkering van medialaan best in de GPV methode? Gewoon het dividend meerekenen dat betaald is (zoals in cashflowstatement)

Of deze eruit halen en waarderen volgens een SOTP?

"Aandeel in het resultaat van geassocieerde ondernemingen en joint ventures"

Dit gaat over verschillende minderheidsparticipaties, waarvan medialaan de grootste vormt. Hoe beoordeel je zoiets best vermits we geen FCF's kunnen berekenen op deze participaties?

http://www.roularta.be/sites/default/fi ... V16_NL.pdf

Roularta owns 50% of Medialaan NV (which operates two TV channels and a few radio stations). Roularta received a total of 11.7M EUR in dividends in FY 2016, but didn’t provide a breakdown. Fortunately the website of the National Bank of Belgium allows you to search for the annual report of Medialaan (which is a private company). Whereas the total dividend upstream from Medialaan was 15M EUR in FY 2015 (30M EUR X 50%), it dropped to 10M EUR in 2016.

https://static.seekingalpha.com/uploads ... _rId11.png

This dividend decrease was undoubtedly caused by the lower net income of Medialaan (a net loss of 4M EUR versus 28.3M EUR net profit), and when I was searching to figure out what caused this difference (after all, Medialaan’s revenue increased whilst its operating expenses decreased), I was extremely surprised by the reason and feel very confident the dividend will increase again as the operating income actually increased by more than 20%.

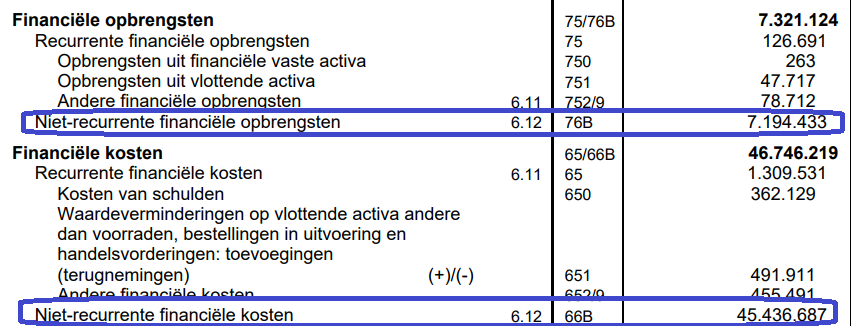

As you can see on the next image, FY 2016 contained 45.4M EUR in non-recurring financial expenses (after digging a bit deeper this seems to be related to an impairment charge), and 7.2M EUR in non-recurring financial income for a total of 38M EUR in non-recurring charges.

https://static.seekingalpha.com/uploads ... _rId12.png

The fun (ahem) thing about this is the fact Roularta was required to pay taxes on these non-recurring charges anyway, and the 17.8M EUR tax bill tipped the bottom line into the red territory. Should I add these non-recurring items back to the equation, Medialaan would actually have shown a substantial profit increase to 42M EUR (+50%) and a dividend payment of 30M EUR would represent a payout ratio of less than 75%. This doesn’t take the additional revenue from Mobile Vikings into account, a cell phone provider which was acquired during 2016.

Maw, dividend van Medialaan was (eenmalig?) laag door eenmalige impairment charges. Zal dit jaar wellicht weer stijgen.

-

anonymous9

Re: Roularta

Noot, ik heb een long-positie en koop maandag bij als er nog zijn die willen verkopen op dit niveau.

Re: Roularta

Thx, helemaal niet bij stilgestaan dat ik de jaarverslagen van medialaan bij de kruispuntenbank kan opvragen

Ik zit sinds begin 2016 long aan €23.

Reclame-inkomsten zakten 1ste kwartaal wel, dus afwachten of het dividend uitkomt op het niveau van 2015.

Ze hebben ook meer dan 2 tv-stations; CAZ, Vitaya, Vtm, Vtm kazoo, Q2... Kanaal Z & WTV vallen niet onder medialaan dacht ik.

btw hebt ge enig idee hoe dat zit met die overdraagbare verliezen (verkoop van franse dochter?) waardoor ze geen/amper belastingen moeten betalen bij print media? De aanpassing van de vennootschapsbelasting voorziet een minimumbelasting dacht ik van 7,5%?

Staat op de balans aan activazijde voor zo'n € 21M als "Uitgestelde belastingvorderingen"

Weegt dat mogelijke 'verlies' van die op tegen de verlaging van de VB die (zeker op termijn) wel gunstig is voor medialaan?

http://www.roularta.be/sites/default/fi ... grvb15.pdf

Ik zit sinds begin 2016 long aan €23.

Reclame-inkomsten zakten 1ste kwartaal wel, dus afwachten of het dividend uitkomt op het niveau van 2015.

Ze hebben ook meer dan 2 tv-stations; CAZ, Vitaya, Vtm, Vtm kazoo, Q2... Kanaal Z & WTV vallen niet onder medialaan dacht ik.

btw hebt ge enig idee hoe dat zit met die overdraagbare verliezen (verkoop van franse dochter?) waardoor ze geen/amper belastingen moeten betalen bij print media? De aanpassing van de vennootschapsbelasting voorziet een minimumbelasting dacht ik van 7,5%?

Staat op de balans aan activazijde voor zo'n € 21M als "Uitgestelde belastingvorderingen"

Weegt dat mogelijke 'verlies' van die op tegen de verlaging van de VB die (zeker op termijn) wel gunstig is voor medialaan?

http://www.roularta.be/sites/default/fi ... grvb15.pdf

-

anonymous9

Re: Roularta

Goede vraag, ik zou eens moeten zien als ik eens tijd heb. Ik herinner me dat er in het jaarverslag van 2016 een note was die de belastingsstructuur analyseerde, misschien staat uw antwoord daar?

Re: Roularta

Best gewoon het dividend meerekenen. Het is een instroom van cash, die in principe duurzaam is. Binnenkomende rente zou je bijvoorbeeld ook meerekenen.Umi schreef: ↑5 augustus 2017, 13:25 Aandeel heeft serieuze klappen gekregen de laatste tijd (na zwakke resultaten een tijd terug) maar gistere nog eens 6% er van af...

Wat ik me af vraag, hoe giet je die dividenduitkering van medialaan best in de GPV methode? Gewoon het dividend meerekenen dat betaald is (zoals in cashflowstatement)

Of deze eruit halen en waarderen volgens een SOTP?

"Aandeel in het resultaat van geassocieerde ondernemingen en joint ventures"

Dit gaat over verschillende minderheidsparticipaties, waarvan medialaan de grootste vormt. Hoe beoordeel je zoiets best vermits we geen FCF's kunnen berekenen op deze participaties?

http://www.roularta.be/sites/default/fi ... V16_NL.pdf

Re: Roularta

Uit nota van KBC over hervorming vennootschapsbelasting:

ROULARTA +8% EPS IN CORE SCENARIO

At its FY15 results, Roularta recognized a total deferred tax asset of €

106m, arising for the most part from the finalized sale of Groupe

Express (tax loss carry forwards of € 311m). After following accounting

rules and offsetting the newly-recognized deferred tax assets with its

deferred tax liabilities, Roularta had booked at FY16 results a deferred

tax asset worth € 21m on its balance sheet for the next 5 years.

Moreover, we believe the company still has around € 54m in

unrecognized deferred tax assets. Given that Roularta’s printing

business would benefit from these tax loss carry forwards in the mid to

long-term, Medialaan is the only activity that would directly benefit from

the corporate tax rate reduction. Given that the tax reform is supposed

to allow tax consolidation from 2020, we do not believe that the printing

business will see its Effective Tax rate increase to 7.5%. We estimate a

positive EPS impact of 6% in 2018/2019, and 8% in 2020. However, the

outstanding DTA will likely be impaired and it is unclear whether the

Belgian gov’t will seek to cap the deductibility of previous tax losses over

time.

ROULARTA +8% EPS IN CORE SCENARIO

At its FY15 results, Roularta recognized a total deferred tax asset of €

106m, arising for the most part from the finalized sale of Groupe

Express (tax loss carry forwards of € 311m). After following accounting

rules and offsetting the newly-recognized deferred tax assets with its

deferred tax liabilities, Roularta had booked at FY16 results a deferred

tax asset worth € 21m on its balance sheet for the next 5 years.

Moreover, we believe the company still has around € 54m in

unrecognized deferred tax assets. Given that Roularta’s printing

business would benefit from these tax loss carry forwards in the mid to

long-term, Medialaan is the only activity that would directly benefit from

the corporate tax rate reduction. Given that the tax reform is supposed

to allow tax consolidation from 2020, we do not believe that the printing

business will see its Effective Tax rate increase to 7.5%. We estimate a

positive EPS impact of 6% in 2018/2019, and 8% in 2020. However, the

outstanding DTA will likely be impaired and it is unclear whether the

Belgian gov’t will seek to cap the deductibility of previous tax losses over

time.

Re: Roularta

Deze stond al lang op mijn lijstje. Gisteren eindelijk een eerste positie gekocht. Recent toch een hoop cash vrijgekomen van verlopen fagron obligatie

Re: Roularta

@ Jens; merci voor de nota!

@ Paljas, ik heb helaas geen cash vrij

@ Paljas, ik heb helaas geen cash vrij

-

nyotaimori

- Sr. Member

- Berichten: 263

- Lid geworden op: 14 aug 2015

- Contacteer:

Re: Roularta

Halfjaarresultaten worden niet gesmaakt: bij opening -8%, ondertussen al wat herstel tot -4%.

http://www.roularta.be/sites/default/fi ... cht_NL.pdf

http://www.roularta.be/sites/default/fi ... cht_NL.pdf

{kind=link}

{kind=link}

Re: Roularta

Erg hoog volume evenwel. Veel verkopers dus.....

Pessimisme is zoals porno, het verkoopt.

-

anonymous9

Re: Roularta

En ook kopers, het ging plots razendsnel van 19.5 naar 20.25 (en weer terug  )

)